What can you do when you need to access eCommerce short-term financing, but you’re not sure what options are available to you? Below are some solutions worth considering.

Ecommerce businesses are some of the most capital intensive online businesses to run. You have large upfront costs – in the form of inventory and ad costs.

Add on that many eCommerce businesses see a significant amount of revenue in Q4 with the busy holiday shopping season, and this means that many business owners have to place large inventory orders months before they ever see the money in the bank.

It is no wonder that many eCommerce businesses turn to short-term financing options to raise necessary funds to keep their businesses growing.

However, banks and VCs are closed to many eCommerce businesses since they don’t have many assets – outside of inventory- and tend to require more and more funding as they grow. The amount of inventory needed keeps getting larger and how many times they need to reorder them more frequently as they grow.

In this post, we’re looking at 6 ways eCommerce companies can access short-term financing, including:

- Why and when you need working capital

- Stop struggling to find a loan structure finance option that meets your needs

- Is self-funding practical?

- What are your options for accessing finance?

Why and when you need working capital

Timing is everything, and never is it more so with cash flow. Expenses need to be paid and inventory needs to be ordered regardless of when cash comes in.

Managing the gap between inventory reorders and when you need to pay employees, contractors, and suppliers is a vital part of managing a business and can bring many businesses undone.

How can you bridge the gap in your cash flow cycle?

What you need are some extra funds to bridge the capital gap until your cash flow stabilises. Share on X.

Stop struggling to find a loan structure finance option that meets your needs

Keep running into closed doors in your quest for funding?

Many small business owners have trouble accessing finance.

Generally, banks require a proven track record of profitability and stability and this can be difficult for start-ups to provide. Accordingly, finance can be difficult to secure through traditional channels, who can be conservative and risk-averse. Many small businesses also lack assets to provide as security which adds to the difficulties in securing traditional finance.

Small businesses can be frustrated by what seems like unattainable requirements to be able to gain funding. Most banks won’t ever say NO. They will say, we can do this (i.e. lend you this) if you do this (i.e. provide 2 years of financials, $X of security… etc)

So what can you do when traditional channels are not the solution?

Start by exploring the possibilities of self-funding.

Is self-funding practical?

The alternative to seeking equity or finance is “bootstrapping” which means you scrimp and save to pump cash flow back into the business.

Bootstrapping can mean that it takes longer to achieve business goals but can be an effective way to manage growth. It can also mean the owners or founders forgo drawing earnings in the early stages of the business so they can reinvest in growth.

Self-funding does have advantages, but it isn’t always viable. Here are some other options.

What are your options for accessing finance?

1. Loans from friends and family

It’s easiest to hit up those you know for money. Treat them with the respect they deserve. Don’t solicit their money without having a plan in place to return their investment.

WARNING: This option can get messy if financial matters complicate personal relationships.

2. Crowdfunding

Fun, debt-free and a great opportunity to boost a new idea. Using crowdfunding platforms like Kickstarter and Indiegogo are particularly great to test the market and get the initial seed funding for new products.

WARNING: Although your supporters give willingly, their funds should be put towards specific projects. Support won’t last long if you constantly beg for capital to fund operations.

3. Invoice factoring

You may qualify for this when you don’t have enough cash receipts to cover expenses but the invoices are out there. A factoring company can pay you a portion of your anticipated income. After bills are squared up, the factoring company gets the loaned money back.

WARNING: High fees can lurk behind an invoice factoring arrangement. The quality of lenders varies a lot – so do your homework! As with all short-term finance, it is typically more expensive than long-term finance.

4. Revenue based financing

One of the newest options available for eCommerce companies is revenue based financing. For example, this structure was popularized by Wayflyer – allows eCommerce entrepreneurs to get funding for inventory and marketing expenses without giving up equity or ownership in their business.

5. Using a credit card

Using a credit card is very common in starting up a new eCommerce business and funding inventory purchases.

WARNING: Using a credit card can be dangerous if you are not disciplined about paying off the debt. Credit cards don’t have structured payments to reduce debt, so it’s easy for this to be neglected. Accumulating debt for your business, without paying it off, can damage your credit score. Many credit cards also have high interest when compared to other funding methods.

6. Brex

Brex brands itself as the financial operating system for the next generation of businesses. They make it easier to see all of your bank accounts, credit cards, expenses, and accounting in one place. In particular, their Brex Card claims to offer 10x – 20x higher credit card limits than traditional business credit cards with no personal guarantee and added flexibility.

7. Amazon Lending

For FBA businesses, Amazon Lending may be another viable option. They provide working capital loans for inventory management, product line expansion, and marketing. The application process is fully digital. Most businesses get a decision on whether or not they are approved within 5 business days of completing their application.

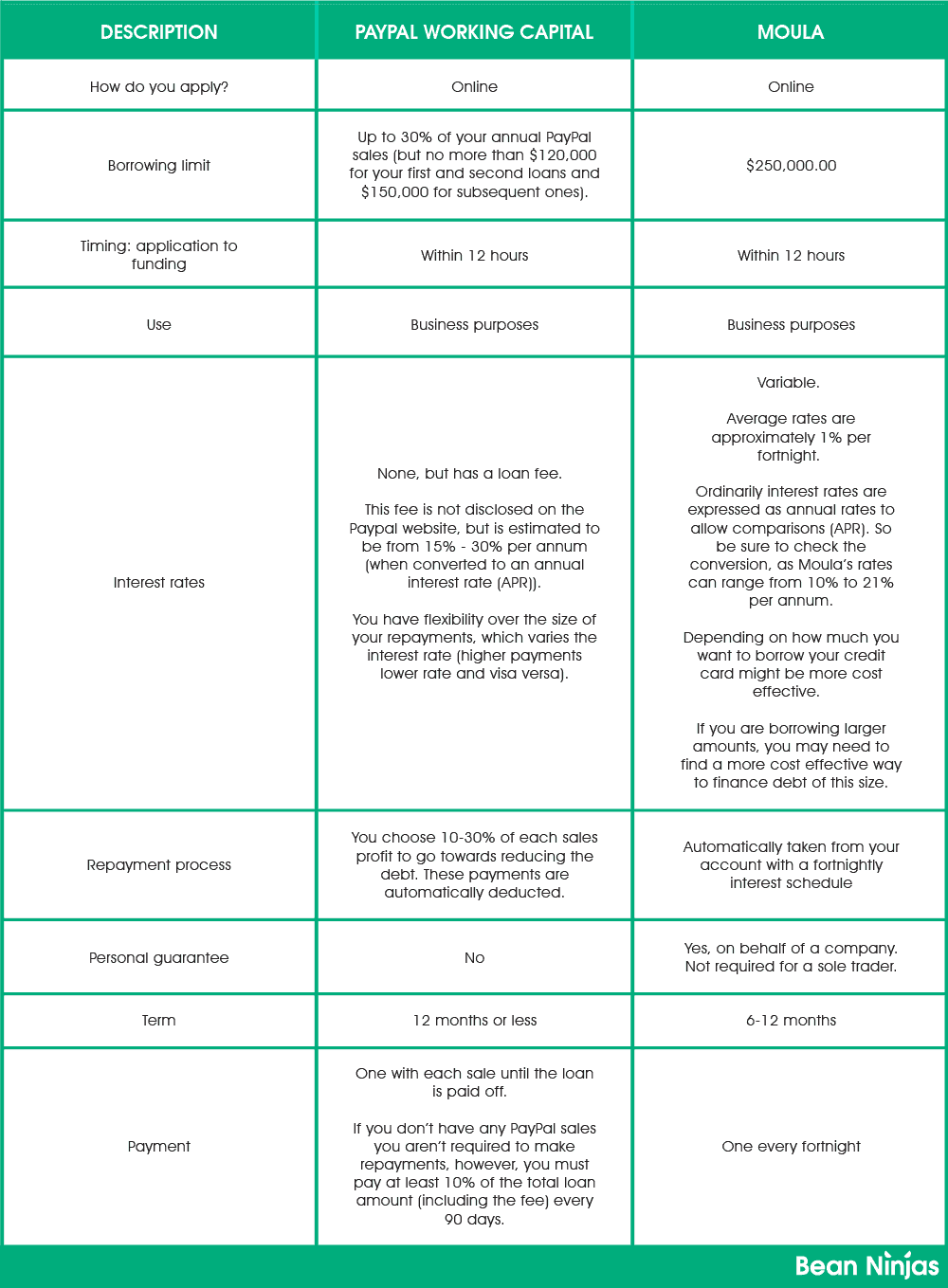

8. PayPal Working Capital and Moula

Both of these companies function with the same premise: putting funding in the hands of small business owners right when it’s needed.

.

Paypal

You could get a business loan through your current PayPal account.

Pros:

- If you don’t have money coming into your business, you don’t have to make a loan repayment at that time

- You can make early repayments

- You don’t need a credit check to be approved for a PayPal loan

Cons:

- The smaller you want your repayments to be, the higher your fees

- You won’t know what your fees will be until you apply

- You must have a solid history of sales in PayPal ($20,000 in a year) to qualify for the loan

- Reputation for poor customer service, however, based on our recent interactions this seems to be improving.

.

Moula loan

Moula provides loans to businesses that have an ABN or ACN, have been in business for 12 months, have more than $5,000 monthly sales and a good credit history. You don’t need a prior account to apply, but this works much like PayPal Working Capital.

Pros:

- High loan amount (up to $250,000)

- You can make early repayments

- Repayment terms are from 6 months to 12 months

- Can connect to your Xero account. Add that to the list of amazing Xero features!

Cons:

- Considers your credit history, so that has to be in good standing

- You will be charged interest on your loan

- Requires a personal guarantee if the borrowing entity is a company

- There are high fees for needing more time to pay off your loan

Related: PayPal Working Capital Reviews

Is there any difference between Moula and PPWC?

See for yourself:

On the whole, PayPal Working Capital and Moula provide two excellent short-term financing options for businesses that can’t or don’t want to access traditional funds

Related: Moula Unsecured Small Business Loan

Choosing between PayPal Working Capital and Moula comes down to how large of a loan you need. Share on X.

To think about before you apply for short-term financing

Short-term financing could be the lifeboat that helps your business stay afloat during tough times. When there’s a gap in capital or cash flow, you may not have another option but to seek an injection of working capital to manage the tough times.

Applying for online short-term financing like Moula and PayPal is straightforward, fast and easily accessible.

As great as companies like Moula and PayPal can sound, there are still some downsides to weigh up.

When you take out a short-term business loan, you don’t have a lot of time to pay it back. How long you have depends on the lender.

PPWC, for example, is flexible in its repayment requirements. But it still requires that the full loan balance be paid off within 18 months. Moula requires the principal amount to be repaid within six months.

The point is: this is short-term finance, it has to be paid off quickly.

You will need to ensure your business can deliver the funds needed to pay back your loan in time. One of the ways you can protect your online business is by planning ahead before taking out any loan.

Is short-term financing right for your business?

All small businesses need working capital to function. But there is no single funding solution that’s right for everyone.

Experiencing a short-term cash flow shortage gives you the opportunity to understand the cash flow cycle of your business. This is valuable information and may prevent further problems in the future.

Things to consider include:

- Understand your cash flow cycle – Do you have a concentration risk? Are you paying your accounts too quickly and acting as your creditors’ bank? Can the cycle be improved?

- Understand what the future looks like is just as important. Is this really just a short-term need? Or is there a long-term issue that needs to be solved? An immediate cash delivery sounds attractive, but it will only pay off if it is part of your larger plan. You need to have an idea of what your cash flow will look like in the future to ensure the shortfall is not repeated, or if it is, that it can be managed and planned for.

When looking at getting a loan, it’s important to be honest with yourself about whether the loan is required to fund a shortfall in operations or whether it is for capital.

If it is to fund operations then it could be an indication there is a flaw with the business model. For example, some business models are only profitable at scale so this could also be the reason, or the business model may need further development.

Do you have a clear view of your cash-flow and financial position so that you can make an informed decision about your business cash-flow needs?

Need a hand getting your figures in order?.

It could be time to get a professional eCommerce bookkeeper on your team. Before you go in search of funding, you might want to get clear on your actual numbers. Schedule a free call and we’ll be happy to help get you started.