A Chart of Accounts is a list of all the Profit & Loss and Balance Sheet accounts

This is a standard accounting system feature when you are using software, like Xero, and allows you to collate all the data into financial reports that can be used by and leaders throughout your eCommerce business.

In this post, we’re sharing what a chart of accounts is and how to customize it for your business (with templates).

Want to save yourself a ton of time and headaches working out how to properly set up your Chart of Accounts (or Xero file), and be trained by a Xero expert? Check out our “How to do Bookkeeping in Xero” online course here.

Why is a Chart of Accounts so important?

It is important because it is designed as a way to separate expenditures, revenue, assets, and liabilities, so a business can have a clear understanding and view of their overall financial health. It also helps meet the needs of management reporting while also complying with all financial reporting standards.

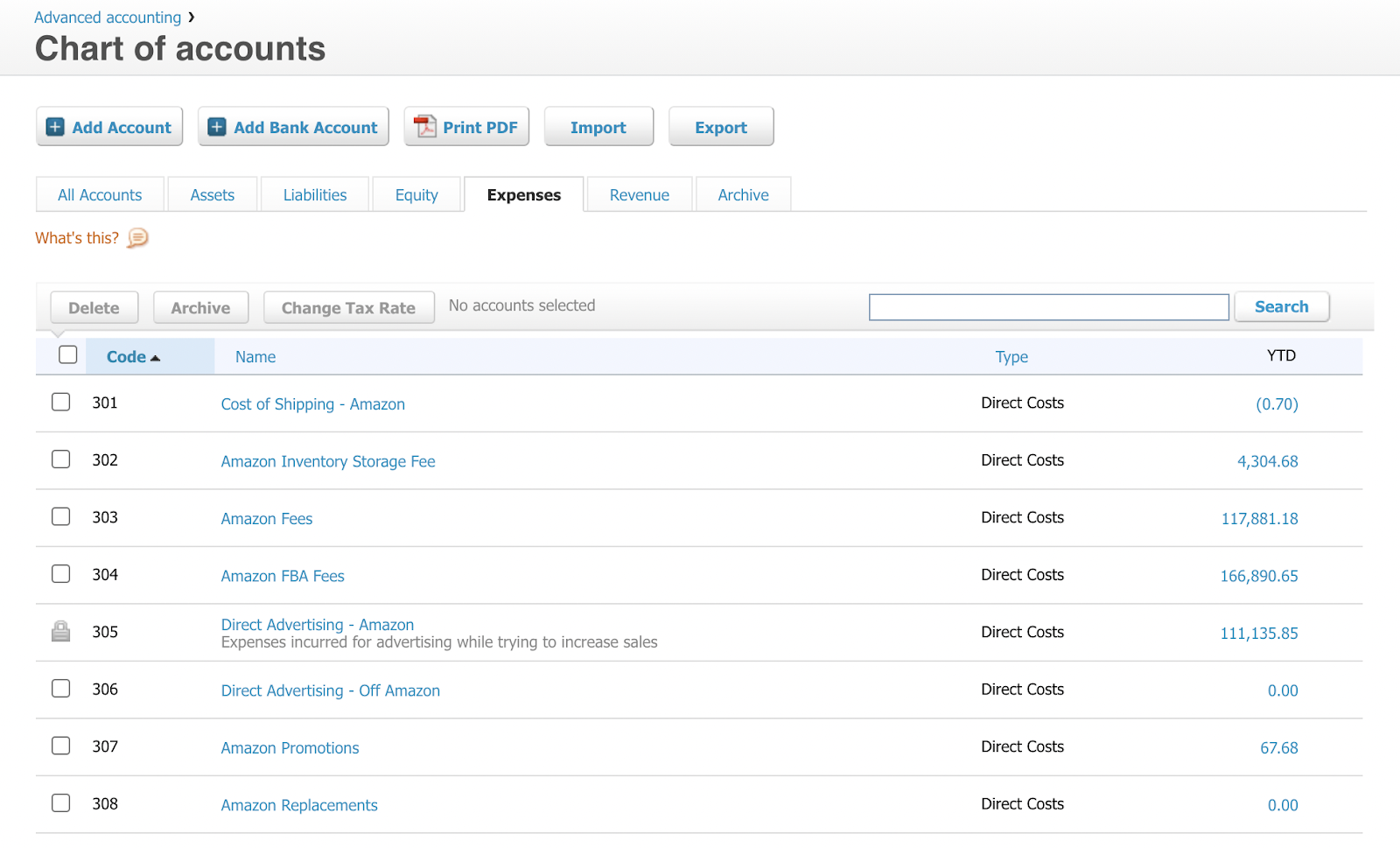

Screenshot below of the Chart of Accounts screen in Xero

Want to save yourself a ton of time and headaches working out how to properly set up your Chart of Accounts (or Xero file), and be trained by a Xero expert? Check out our “How to do Bookkeeping in Xero” online course here.

What is a chart of accounts?

The standard Chart of Accounts allows you to allocate every transaction to a category in your general ledger so that you can see a complete list of sales and expenses.

When you set up your financial accounting software, it is important that you customize the Chart of Accounts to the needs of your specific business.

Standard categories in a Chart of Accounts will include:

- Assets

- Cash and Cash Equivalents like Bank Accounts, Accounts Receivable, Inventory.

- Non Current Assets such as: Fixed Assets like Office and Computer Equipment

- Liabilities

- Current Liabilities such as Short Term Debt like Credit Cards & Shopify Capital Loans (as these are paid back within 12 months), Accounts Payable, & Tax Liabilities

- Non-Current Liabilities & Equity such as Retained Earnings, Current Year Earnings and Owner Contributions/Drawings

- Equity

- Revenue

- Expenses

Each of those categories will have sub-categories listed. For example, the expenses category might include . . .

- Cost of goods sold (COGS)

- Payroll / Salary Wages

- Software Subscriptions

- Bank fees

- Travel expenses

- Marketing Expenses

There can be significant differences based on the type of business you own.

For example, if you run a DTC eCommerce business on Shopify, you’ll want to clearly see your top-performing and worst-performing products in your chart of accounts layout. Whereas, a client service business will want to see aged payables and aged receivables.

Note: It is important that you have a consistent coding system for your Chart of Accounts, particularly if you have multiple people in your accounting software (such as a tax accountant, bookkeeper, virtual CFO, you, and your senior management team).

You need to have a very specific description of which transactions should be coded to each category so that your data is consistent over time. For example, differentiating and posting transactions relevant to Cost of Sales and Cost of Goods Sold (product costs, fulfillment, postage and shipping, merchant fees) appropriately to have clear Gross Profit Margins.

The whole point of categorizing financial transactions like this is so that you can make comparisons over time that allow you to make data-driven decisions as your business grows. If you don’t have consistent record-keeping, you’ll be relying on data that could be inaccurate, which in turn results in poor financial decisions that can hamper your growth.

For example, these inconsistencies can show up in your Balance Sheet. Your balance sheet is like the highlight reel of your business, and show the following:

Assets – These can include Inventory (both on hand and in transit), prepayments for supplier deposits or machinery necessary to turn raw materials into finished goods and even cash held in your bank account or more intangible assets like trademarks and patents.

Liabilities – This is a record of all the debts owed by your company. Often you will find the word “payable” in this category like accounts payable, wages payable, sales tax payable, and invoices payable. This can also include income tax, credit card balances and remaining balance owed on working capital loans.

Equity Accounts – This is what is left after the liabilities have all been subtracted from the assets. It is often considered the measurement of how valuable the business is to its shareholders. It is a clear outline of the shareholders’ equity and stock.

For example, if you believe that loan payments fall into liabilities, but your bookkeeper has been logging those payments in your expense category, then you’re unable to make accurate decisions about either category and will likely be pulling your hair out trying to work out why your liabilities are not decreasing while your expenses seem very high.

Is the Chart of Accounts similar to a balance sheet?

Not exactly. The Chart of Accounts actually begins with the balance sheet accounts and then is followed by the income statement accounts. The accounts will stay in the same order as they are presented on the financial statements.

A balance sheet is a statement listing the assets, liabilities, and capital of a business at a specific point in time and then details the balance of income over an earlier period of time.

How to customize your chart of accounts

Customizing your Chart of Accounts can help give you more meaningful financial data. Instead of KonMar-ing your house … how about your Xero file?

As your business evolves, it’s important to review your Chart of Accounts to ensure it is still relevant. In this short video, I share a few tips.

Take action: review your Chart of Accounts to see whether any accounts need to be created /archived or edited to more accurately reflect the transactions in the account.

Adjusting Your Chart of Accounts

You can add as many accounts as you want throughout the year, but you should never delete any old accounts there are until the end of the year, or it could mess up your books and cause problems.

If changes do need to be made, it might be best to record it under a new account for that particular item or category rather than recording it in the regular expense account area it would have initially been put. This can help keep things adjusted properly without messing up the numbers in other categories throughout the year.For example, let’s say you started the year with one advertising account but became interested in optimizing your spend to the channels generating the largest returns, so you split them out into individual expense categories such as Advertising – Amazon, Advertising – Facebook, etc. Then a charge comes through for a new advertising channel you’re exploring like Pinterest, rather than post to your original advertising expense account you might consider adding a new account called Advertising – Other.

***

In summary, a Chart of Accounts is a tool that provides a business with a complete and accurate listing of each account in their general ledger. These accounts are broken down into different subcategories. It is a good way to organize finances and give shareholders more insight into the financial health of the company overall.

Having a Chart of Accounts for your business also makes it easier to locate specific amounts. Each account will have account names, a brief description of the account, along with an identification code. A Chart of Accounts can be customised to fit the company’s specific operations.

Additional Chart of Accounts FAQ

What is included in a Chart of Accounts?

Typically, you will find assets, liabilities, equity, revenue, and expenses in a Chart of Accounts. Revenue and expenses are usually listed last.

How is a Chart of Accounts grouped for reporting purposes?

The Chart of Accounts starts with cash, goes through to liabilities and shareholder’s equity, and then moves on to accounts for revenue and, finally, expenses.

What types of accounts are assets and liabilities?

Every business has a list of assets and liabilities. Asset accounts include cash in hand, cash in the bank, real estate, inventory, prepaid expenses, goodwill, and accounts receivable. Liability accounts, on the other hand, are different financial obligations and often include accounts payable, bank loans, bonds payable, and other accrued expenses.

Need help with your Chart of Accounts?If you’ve got questions about how to setup Xero or structure the Chart of Accounts for your specific business, schedule a free call with the Bean Ninjas team here.