Want to learn how to unlock cash flow through automation and apps? Find out how with our guest Twyla Verhelst.

In Episode 84 of the Bean Ninjas Podcast, Bean Ninjas COO Wayne Richard talks to Twyla Verhelst about unlocking cash flow through automation and apps.

(Source: https://www.facebook.com/twyla.verhelst)

Episode Highlights

Why do most businesses fail? Poor cash flow management and forecasting. Twyla Verhelst tells you how to avoid these traps Share on X00:45 – Twyla’s diverse background starting out as a CPA and starting her own businesses

02:20 – How Twyla identified the gaps in skill sets that existed in the bookkeeping and accounting industry

04:45 – What Helm is and how it can help you with cash management and forecasting

08:00 – Identifying the pain point that all bookkeepers, business owners and accountants shared which lead to Helm

09:33 – Top 3 considerations for anyone thinking of launching a software business

14:50 – Tips about Cash flow forecasting and cash flow management.

15:58 – Why you shouldn’t pay too fast and collect too slow

17:59 – Why Helm was excited about Xero’s new cash flow dashboard feature (even though Xero is a competitor!)

23:00 Having a voice and supporting diversity in the accounting industry

29:00 – What financial freedom means for Twyla Verhelst

Learn the foundations of financial literacy and using Xero with Meryl.

Transcription

Unlocking Cash Flow Through Automation and Apps with Twyla Verhelst

Announcer Welcome to the Bean Ninjas Podcast, where you get an all-access pass to see what happens behind the closed doors of a fast-growing global bookkeeping and financial reporting business.

Wayne Richard:

Welcome to the show, Twyla. How are you doing this morning and where are you recording from today?

Twyla Verhelst:

Thanks, Wayne. I’m doing great and I am here in Calgary, Alberta, Canada.

Wayne Richard:

Awesome. So share with our listeners a little bit about yourself and your career path.

Twyla Verhelst:

I have a bit of a meandering career path to be totally honest with you. I’m a CPA; somebody that is kind of not your traditional CPA. And after I finished up my designation, I got my first controller job, found myself really wanting to get into my own type of business, took a few different ventures within having a mortgage brokerage, doing some recruiting for accountants and some bookkeepers. And then now, I have landed back into the accounting space as well as in the software fin-tech space.

So it’s definitely an abnormal path, to say the least. But I like to say that the diversity of my path has brought me to where am I today and been able to give me a lot of different pictures and different skill sets along the way to bring to kind of what we are up to now, which is having our accounting and bookkeeping firm as well as then, Helm, our software company.

Wayne Richard:

Awesome. And today, you’re going to share with us some tips on unlocking cash flow through automation and apps. So firstly, I love your mission of empowering bookkeepers and accountants to create the business they desire using these tools such as the apps you’ve created and also workflows along with the most invaluable and intangible tool, their authentic self. So when did you first realize this was your mission and what was happening at the time?

“Software is hard” as per Jamie McDonald” Twyla Verhelst, Helm. Share on XTwyla Verhelst:

You know, over the past year and a half since we’ve started down the journey of creating a cash flow forecasting and cash management tool, it’s enabled us to work really closely with other accounting professionals all around the globe. And during this time, I got really conscious of what it is that we are trying to do with the tool, but also the gaps and the skill set that existed in the industry.

And so, within our own accounting firm, we are 100% cloud-based, we have embraced technology as much as we possibly can in order to deliver an experience for our small business clients that’s really a value add and we hang out a lot in that advisory space while we let apps do more of the bookkeeping space.

And so, there are two components ultimately to delivering a client experience, an experience that they can’t imagine ever living without, and that’s the tools that we’ve now got at our fingertips as the tech and software space is so rapidly moving forward and so progressive. As well as our own self; I mean, at the end of the day, you can use all of the tech that you want, but you still have this human experience with another human, that being your client.

And so, to be able to actually recognize what it is that you can give as a human and yourself back to that client, that small business owner coupled with the technology, that’s really kind of what got cleared to me over the past year and a half as we started to work with more accounting professionals, as we began to do more testing and roll-out of Helm, the cash flow forecasting tool.

Wayne Richard:

It’s interesting, the transition, it seemed as so it’s becoming where the bookkeeping piece is about 80% of data in tech, and about 20 if not less than % individuals making insightful decisions and making judgment calls. Where advisory is now moving us to a place where really the 20% is the data, the good clean data you’re getting out of that bookkeeping, and 80%, those decisions, assumptions, and plans around what you want to see and occur within your business going forward.

So quickly, what is Helm and how did the idea for an app come about?

(Source: https://www.takethehelm.app/)

Twyla Verhelst:

Helm is a cash flow forecasting and cash management tool, and really, it came from inside of our own accounting firm. I mean, truth be told, I never expected to be in the software space. It was not; If I kind of look at 20 years on to my career, it would never have been here. But what happened was, we have a really early adopter of the tech, which meant that we were able to spend more of our time in that advisory space. And I use that word kind of loosely because it’s such a buzzword and it’s that 80% kind of more the human; like you said, and the 20% more of the apps in that portion of what you’re giving back to your clients.

And we spent our time in that space and a lot of that has been because we all know the stats around 80% of small businesses fail, and that most of those failures are due to lack of cash flow forecasting and lack of cash management.

And so, this has been a key component to what we’ve always delivered to our small business clients because we work with clients who are either fast-growing or they’re brand new or they’re subjected to industry trends, where in Alberta, we’re subjected to oil and gas and what’s going on with that market.

And so, we’ve always sat in that space within advisory to manage their cash and do cash flow forecasting for them in order to help them succeed. And so, for us, we found that we were trying to use the tools that were available and we’re finding them to be not fitting our needs. So when you got all this automation within bookkeeping, it seems so interesting to us that it all kind of stopped, hard stopped, at the point of reconciling your accounts within your accounting platform to then saying, “Okay. Well, now I’ve got to figure out our cash flow before I run, suggest their AP and run those payments.”

And that became very manual for us. We couldn’t find the tool that was going to be granular and precise enough for us to actually make decisions off of in terms of, “Are they going to run out of money? Or do they have enough? Or can we really suspend their payments?” So we kept using excel.

So as we were stumbling through using excel, don’t get me wrong, excel works very well for this purpose, but it’s time-consuming. It’s hard to scale it because of that; it’s error-prone, let’s be honest. I mean, put a negative where there should be a positive, but now your cash flow forecast is completely wrong.

And it’s not always current. So you do the cash flow forecast and then, instantly, you run some payments or you collect from some customers, now you need to start it over again. And so, we decided to venture down the path even for within our own firm of creating something that’s more automated, but also more visual for the clients so that they can see what’s going on and then not kind of going out blindly, “We’ll trust in the spreadsheet.”

And so, as we went down the path of creating the tool, then we started to put it out to others in the market, and that’s where we started to go globally to other accounting professionals saying, “Look, this is a pain point for us. Is it a pain point for you?” And quickly, we learned, it is a pain point for other people.

Either they’re trying to do what we’ve been doing, which is using excel or something more cumbersome, or that they’re not offering this as a service to their clients even though they’ve realized that cash flow is extremely important and they’re clients who have been hinting that needing cash flow management within their services from the bookkeeper or accountant.

But they’re not doing it because of the fact that it’s not efficient. And then, when it’s not efficient, it’s hard to get your small business owner to pay for it because it’s high cost because it takes too long. So we started then to do more testing within the market, globally.

And as we saw that there was more and more positivity around the idea of everybody having this tool, it really got us excited because, at the end of the day, we’ve been helping small business owners for years. And so, if we can put it tool into accountants and bookkeepers’ hands to help their small business clients, then now that impact of helping small business owners has gone even further, the reach is further because it’s going through the accountants and bookkeepers.

Since we started down the journey of creating a Cash Flow and Cash management tool, it’s enabled us to work really closely with other accounting professionals all around the globe.

Wayne Richard:

So you shared a bit about why you’ve created the tool as essentially in each that you felt the need to scratch within your own firm. And then also, a little bit about testing with others. Could you share maybe your top three considerations for anyone thinking about getting into the software? And what are some of the things that they need to look out for before jumping in?

Twyla Verhelst:

I chuckle at this because a quote that’s really stuck in both my head and Kelvin, my business partners’ head has been something that we heard probably about a year ago now from Jamie McDonald, one of the founders of Hubdoc.

And his exact words were, “Software is hard.” And I respect the fact that we’re the only kind of like tip of the iceberg here now with where we’ve gone so far with Helm. He’d probably laugh at me at this point saying, “Gosh, girl, you haven’t even experienced the hard part yet.”

But it’s something that really resonated with us to know that it is hard and it’s extremely fast-paced. You have to be kind of always looking numerous steps ahead in terms of what could be coming or what could be useful in the future. And it’s very different from running an accounting firm.

For me, it’s been a case of even something as simple as coding or fixing a bug. I don’t know how to code; I’m an accountant. And whereas, in our accounting firm, when something went sideways and we need it all hands on deck, I could contribute. I could go back to reconciling banks, I could do data entry if I needed to, I could manage payables; whatever that look like.

But in a software company, I can’t do that. I can’t do anything about fixing a bug other than to liaise with the end-user and our dev team. So that’s definitely something to consider, it’s just a control thing and it really made me aware of how much I like to be able to be in control and being able to fix something as soon as something goes sideways.

It helped us, on the flip side, in terms of really understanding the pain points and that would be something that I would give as the top consideration to someone who’s looking at software is really know the pain point they are trying to solve inside and out. And we have that advantage, we came up with the idea of Helm from our own pain point.

And so, we know exactly what we’re trying to solve. But that said, we’ve also been open to ideas and possibilities about what other people’s pain points are, which you have to be super cautious of and this is something that we’ve also been given for advice that I would happily pass along to somebody else is to just be mindful that you don’t go down the path of chasing what people like to call the unicorn features where it’s something that somebody brings to you as a user saying, “You know what you need to put in here in your app is this.”

And it sounds really awesome, but the reality is there are a group of users that really need that or is that really an edge case where it’s something very specific and very unique to a particular client or industry or a customer need. And so, you really have to watch that. So it’s kind of this balance of knowing what it is that you’re trying to solve and be really true to what that solution is that you’re trying to provide.

But be open to the possibilities and ideas that other users are bringing forward, but yet, still be mindful of the fact you could go down the rabbit hole and create a feature and spend a lot of time and resources creating a feature that the majority of your users are going to see no advantage to having. So those are kind of be my top considerations starting with that software is hard as per Jamie McDonald.

Wayne Richard:

That’s great. And I also can imagine that most of those early users are going to be super eager about this type of tool because they’re aware of that pain point. But it could be much different for once traction is gained and acceptance within the tool has started where the needs of those earliest adopters might not be exactly the needs of the majority.

Twyla Verhelst:

Yeah. Great point. And in this industry, we’ve got a variety of different skill sets across bookkeepers and accountants and a variety of different needs that they have based on what their services that they provide to their client. So you’ve got that broadness in of itself coupled with the broadness of how each person does their own accounting, how you record prepaid expenses might be slightly different than how I record it even though in the eyes of compliance, we’re both still on side.

And so, there can be those differences, there can be industry differences, there’s so many differences that everybody who have with what they need from the field, and what that can mean that when you’re trying to kind of create a tool with a broad stroke that covers as many pain points as possible while not getting distracted by one or more of those items.

Twyla's Verhelst’s cashflow management tip: A lot of times... it’s not always that you don’t have enough money, typically it’s timing - it’s a cash gap as opposed to a cashflow problem. Share on XWayne Richard:

So you’ve become an expert in the area of cash flow forecasting. What are some lessons or tips that you’ve learned about cash flow forecasting that you can share with our small business listeners? And are there any practical, quick wins or low hanging fruits where you would instruct them to look first when trying to maximize their cash flow?

(Source: https://www.facebook.com/twyla.verhelst)

Twyla Verhelst:

Yeah. I mean, if I start with kind of the first thing that I can share with a small business listener, it would be to actually view your cash flow forecasting. And so, I have a client specifically, who, to this day, tells me, even though she has banking access; obviously, it’s her company; she does not look at her bank account. And she said it’s because it stresses her out.

They’re a fast-growing company and she just doesn’t want the stress of looking at it. It makes her uncomfortable. That tends to be human nature is it; if it’s scary or makes us feel anxious, then, we don’t tend to look at it. And that then contributes to why 80% of small businesses fail because they don’t have the optics.

Because a lot of times with cash flow forecasting and cash management, it’s not always that you don’t have enough money. Typically, it’s timing. It’s a cash gap as opposed to a cash flow problem in terms of you don’t have enough. You have enough, it’s just the timing. And typically, what small business owners tend to want to do is pay too fast and collect too slow.

So depending on the industry that they’re in, there can be opportunities where the instant that you get a bill in your door, you’re like, “I just want to pay it. I just want to get it out of my mind and not have them bother me that they think that I haven’t paid on time. I want to get a good reputation with this vendor.”

Totally understand that motivation, but can happen is now you’ve paid that too early and you’re collecting from your client or your customers later. And a lot of times, when an invoice that you’ve issued to your customer goes past due, we’re hesitant to call on it. We don’t want to bug them, we don’t want to sound like we’re being needy or that we’re a pain in the butt.

But what happens is that then that creates our cash gap. And even within our own accounting firm, we’re often guilty of it if we aren’t pre-billing or collecting very proactively because you’ve got to pay your people, you’ve got to pay your rent, you’ve got this cause upfront, but then you’re not collecting till later.

So those are the kind of the biggest things is firstly, to get the optics around that and what your cash flow forecasting looks like. And because with that cash flow forecasting information, then you can manage the cash appropriately. And that can look as simple as not paying this vendor this week, paying them next week. And now, you have enough money to cover payroll next week or rent on the first.

And then, if you aren’t the one who’s wanting to do that, it would be to make sure that you bring somebody into your team that can outsource accounting professional or a bookkeeper that is going to provide that service for you because it makes a world of difference. And then, to just be mindful of that general thing that happens is that people pay too fast and they collect too slow.

Wayne Richard:

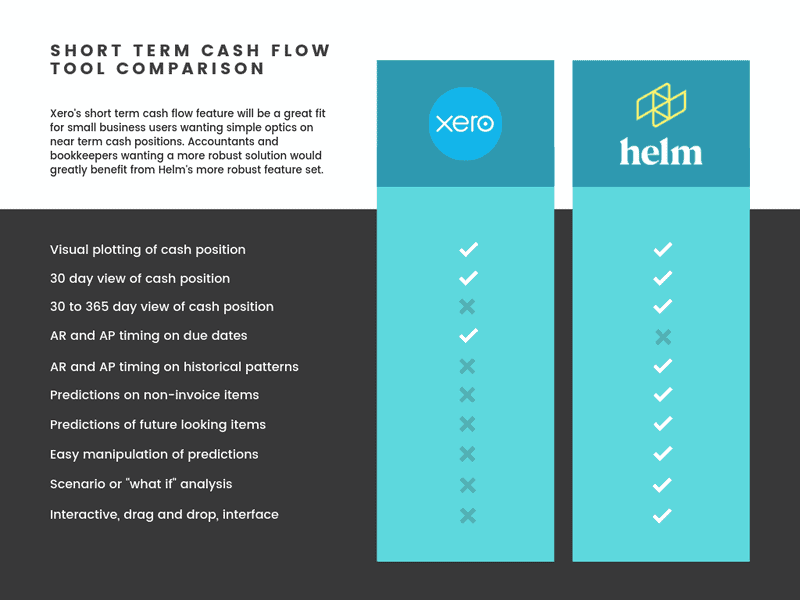

So with that, Xero recently announced their short-term cash-flow feature at Xerocon. Can you tell our Xero listeners what this is and why you might be excited about it?

Truth be told, I never expected to be in the software space!

Twyla Verhelst:

Yeah. It’s funny when that announcement came out, we shared how excited we are about it and it kind of got this mixed reaction from both our accounting colleagues as well as small business users who say, ‘Why would you be excited when they’re potentially competing with you?” But what made us so excited about it is that it was validity that it’s important.

It’s important to small business users that they have cash flow forecasting and that cash and cash management are top-of-mind for our small business users, our accountants and bookkeepers as well as then the people at the accounting platforms like Xero.

And so, when that came out, we were just excited to know that Xero gets it in terms of they have put some resources into this to develop a short-term cash flow dashboard within Xero. So obviously, if they’ve put some resources into it, they know that that is important.

And then secondly, it can start to create some dialogue between a bookkeeper or accountant and a small business owner around the cash flow. So it’s kind of that idea of don’t ignore it, don’t be like one of my clients who doesn’t want to look at it. Luckily for us, for her that we were engaged with her and we just manage it for her so she has that opportunity to do that.

That’s not everyone’s situation. So to see that dashboard of what the short-term cash flow looks like can prompt conversations. And what Xero has released at this time is a 30-day forecast that essentially is your opening bank balance, your existing AP in the system and your existing AR in the system.

So it’s fairly limited at this point in time. So for us, what makes us excited is if it starts to create that dialogue between an accounting professional and the small business owner, then they can start to say, “Well, this isn’t super robust. So, now that it’s brought to my attention, let’s provide that as a service to the small business owner and go down that path of being able to add more value and ultimately, create a different relationship with your small business client.”

So we are super excited about it. We’re excited that Xero sees that important and we’re excited about the spin-off of dialogue and interesting cash flow that’s just naturally going to create.

(Source: https://www.takethehelm.app)

Wayne Richard:

I can see the parallels. I think being a Xero user for some time, they always had visibility, even within the dashboard. You could see at the highest level money’s in against money’s out and you could get a sense of the trends from a month’s perspective. So it seems as though, they’re just really leading further into the conversation in really providing a great hand over to you guys.

Twyla Verhelst:

Yeah. I mean, that’s a great way to put it. I mean, historically, the accounting platforms like Xero have; you’re right; they’ve had dashboards, but it’s been on historical information. And this is kind of one of their first ventures into what is forward-looking look like. And that’s where within our accounting practice, that’s where we lived.

The historical information test is almost the necessary evil. You need to have that timely, current, clean data in order to project going forward. So they have always had those dashboards, which have been helpful about, like you said, trends and seeing kind of what’s up there and what’s down.

And now, this is their first kind of dipping their toe into seeing what does it look like if we do something a lot of bits more forward-looking and see, let’s be honest, they’ll be checking to see what kind of response they’re getting from their user base to see is this a tool that’s going to make sense for accountants and bookkeepers and small business clients.

Wayne Richard:

Awesome. Now, Twyla, I want to switch gears a little bit. You’ve gone down, publicly shared quick, vulnerable and I’d say, the experimental path to increase comfort and confidence as a woman in our industry that really is not one that’s been totally diverse or inclusive at all levels. What made you decide to go down that road?

Twyla Verhelst:

That’s been an interesting journey that I never expected to be on because it really just happened upon me when I got the opportunity on International Women’s Day earlier this year to be on a panel of accounting professionals speaking about women in this industry on International Women’s Day.

And on that panel, even though we were all talking about how we want to see more diversity in this industry, we wanted to be more balanced not across, not just gender, but race, capabilities, etc. And so, as we’re sitting here talking publicly on a live panel event on the internet, I am so darned nervous.

I just, even though I felt so prep, I was just so crazy nervous. And as I got off that call or off that panel, I’ve really kind of reflected really quickly to say if I want to be given the opportunity to take the mic or have a seat at the table in order to create more diversity in this industry, then I better have earned that spot and I better be comfortable in that spot.

Now, that it doesn’t mean that I won’t be nervous in that spot, but I need to be more comfortable and really communicate more clearly and have a voice when I’ve got that opportunity if I want to be part of the change to create more diversity.

So it was literally the day after that event that I created what I now call The Video Per Day Experiment, which essentially was 30 days in a row doing one minute videos per day and posting them on to social media.

And the requirements were just that. It was nothing more than that. There was no requirement about what you spoke about, no requirement about where you were located when you took the video; nothing. It was just, get your phone, record the darn video and post it up to social media and just see what happens, which is why I called it an experiment. Let’s see what happens with 30 days of trying this.

And over the course of that 30 days, it really became so exploratory. I learned so much about myself, my habits, the tendencies I have when things get tough, when I don’t feel like doing it anymore, what it felt like to release some of that vulnerability even though I was still uncomfortable, etc.

And so, I started to get feedback from people who had been watching the videos, which contributed to the experience as well, got to the end of it, challenged myself to sing on camera, which, gosh, thank God, that’s over with. But I want to throw it out there to say, “Okay, I’ve actually got more comfortable, so what can I do to up the bar?”

And what happened with that was it was so exploratory that I felt like I had learned all these lessons and I was really complete with it. And then about, gosh, it was in the end of July that I was on a webinar and I asked somebody for feedback on this webinar, “Hey, how did it; what did you think and how did it go?” And the response from this person who I respect a lot said, “It was alright.”

And that instantly, I thought, “Jeez. I’ve been working on my public speaking and my presentation skills for a number of months now. Alright, it’s time to go back to the drawing board and up the game and do a different experiment.” And in that process, I then actually put it out to others, “Hey, I’m going to do this experiment. I’m going to change it up a bit this time to make it more challenging for myself.”

And what happened is that people decided that they want to jump on board with it, which was a completely different experience altogether. In August, starting at the end of August, we had 35 people do the Video Per Day Experiment, which was absolutely fantastic and really was something that I can’t even put into words what that was like to see others go in that journey.

For me, financial freedom is more to figure out something you are truly passionate about and what you have been put on this earth to do, that is also financially contributing back to you and your family

Wayne Richard:

So are there any particular stories from that month that were encouraging to you and made you think, “Yes. Like, I’m definitely doing the right thing. I’m on the right path.”

Inspired by the @ignitionapp #WomenInAccounting initiative & the #iwd panel led by @madelinekpratt I decided to put myself (the introverted accountant) in front of the camera for 30days to explore women’s confidence. The experiment turned into SO much more and ended with this 🎶 pic.twitter.com/mPhI1GMu60

— Twyla Verhelst (@helm_twyla) April 9, 2019

Twyla Verhelst:

Yeah. You know, this industry is so interesting because naturally, accountants and bookkeepers attract people who are introverts and I’m one of them; I won’t lie. I certainly enjoy spending time with people, but I also enjoy some time to myself. And if I’m going to be contributing to the diversity and a more balanced industry, then I need to recognize what it is that I am going to contribute to that.

And we all have different roles in our contribution if we want a more balanced industry. And some of those rules can look like, “Yup. Be the one who takes the mic, who, even though you’re scared, you are going to do it anyways and you’re going to represent for whether that’s gender, race, or whatever that is.”

And there are other people who are going to play a support role and a cheerleader role, and that role can be just as powerful as the one who takes the mic, because the one who’s taking the mic probably is feeling nervous and scared and can use the support of just the general group to say, “Yup. You did it and you’ve got our back and we need you up there.”

And so, through this journey of not only doing the experiment myself; but then, I’ll say loosely mentoring and supporting others doing it, it became really clear that there is these different roles that we all need to play in order to make this change in terms of more balance in the industry and recognizing that we’re all, to round is that we’re all more similar than we are different and that we all have similar tendencies in terms of nervousness or in terms of not wanting to feel vulnerable or having this desire to have perfection before we take on any sort of challenge or risk or whatever.

And once we recognize it we’re all kind of in this together and that we are all collaborative, it actually can be super powerful. And as I saw some people going through that experiment and blossoming and becoming more confident and really putting their voice out there and finding their voice that as an introvert may have been really deep inside of them, that is so, so inspiring as an industry to be able to see that and then as a woman in this field.

It’s just; I can’t, I can’t even explain it. It’s just something that is a movement that you can see the shift and it’s really exciting.

Wayne Richard:

It’s great. And Twyla, we’re coming up close to time and I just want to commend you for being a leader in that as well. One question we’d like to ask our guest is what does financial freedom mean to you? So on a scale of 1, meaning just getting started, to 10, being entirely financially free, how far away do you feel you are against your goal? And is this even a goal for you?

Twyla Verhelst:

Yeah. This is a great final question, Wayne, and it must have been the trick question and I will struggle to put it on a scale. I mean, if anyone knows me well, they know that I can’t really sit still for very long. So although financial freedom instantly goes to thoughts of a dollar sign or retirement or sitting on a beach and just relaxing, the reality is that although that seems super appealing on the busiest, most chaotic days, I highly doubt I would be able to do that for very long.

And that place in nicely to the fact that about ten years ago, my life changed significantly when my daughter who is nearly two at the time was diagnosed with autism. So in the past ten years, I’ve gotten really realistic with what her financial needs are going to be long term. And so, to take that person who doesn’t want to sit still and couple that with having a child where, as a parent yourself, you know that you want to provide for your child and you want to be able to do what’s best for them and set them up for success.

So for me, I don’t think that financial freedom will look like a dollar sign. I think I’ll probably be working for quite some time. But really, for me, financial freedom is more to be able to figure out something that you’re truly passionate about and what you’ve been put on this earth to do that is also financially contributing back to you and your family.

And so, to be able to do something like that you are passionate about that is rewarding and then be able to that as work, what will happen is it doesn’t feel like work. And I’m incredibly fortunate in that right now, the job that I have does not feel like work. I absolutely love what I do. I get to work with people who are super motivating, very inspiring, uber-smart, and I’m very, very lucky that that is my every day and I’m able to contribute to two industries that are really kind of making some waves and some movement and that’s the accounting and finance industry as well as the tech industry.

So I’m lucky. I feel like I’ve got some financial freedom right now and that I’m able to do something that I feel really compelled to do and it’s really inspiring and just doesn’t feel like work.

(Source: https://www.facebook.com/twyla.verhelst)

Wayne Richard:

That’s awesome. Thanks again, Twyla, for joining us today.

Twyla Verhelst:

No problem. Thanks so much for having me. This has been fun.

Wayne Richard:

Take care.

Meryl Johnston:

Thanks for listening to the Bean Ninjas podcast. Here is three ways to grow your freedom business faster. Number one, download our free Xero Small Business Toolkit. Go to beanninjas.com/podcastgift and use our cash flow forecasting template as well as the other resources available.

Number two, subscribe to this podcast. Don’t miss another episode as we’ll be bringing you more inspiring guests, small business finance and Xero tips and also an inside look at how we are growing Bean Ninjas into a global brand.

Finally, they say the best way to retain what you learn is to share or teach what you’ve learned with someone else. So leave a review on iTunes with your key takeaway from this episode.

Alternatively, you could also post and share this podcast on social media. Be sure to tag us @beanninjas or use #beanninjas on LinkedIn, Facebook, Twitter, or Instagram. This will help us to grow our community and help even more small business owners to create freedom through stress-free finances.

So once again, download, subscribe and share that link again, beanninjas.com/podcastgift.

Catch you on the next episode.

Contact Twyla Verhelst:

- Twyla Verhelst’s twitter

- Twyla Verhelst – takethehelm.app

- Twyla Verhelst’s Linkedin

- Twyla Verhelst’s facebook