Most online businesses start out as a one-person operation. At the beginning, the founder is the salesperson, project manager, accountant and expert all rolled into one. It’s exhilarating, but after a while most of us realize that we need some extra hands.

As the business grows, one of the earliest functions many founders decide to outsource is financial management. It’s understandable — this can be a complex area that requires a lot of attention, and sometimes a level of expertise that is not realistic for the founder to develop themselves.

Some founders will just hire a VA to keep track of their expenses and revenue, but if the VA doesn’t have accounting experience, this can cause problems within the first few months.

To save you finding this out the hard way in your own business, we’re going to break down the functions of an accounting team for an online business, and to give you a few options for setting up your own financial dream team and accounting systems. Note: Not all businesses need a whole team, but there are several incarnations an accounting set-up can take, and you need to find the version that is the right fit for where your business is currently, and where you expect it to be.

.

What Is The Role of The Accounting Team?

First things first: the role of an accounting team is to meet the compliance requirements your business is subject to in the territory you operate in (this can include sales tax, income tax and so on).

The next important role of an accounting team is to provide the business owner with accurate financial reporting and data for decision making. They need to be tracking transactions on a daily, weekly or monthly basis in the accounting software and allocating these transactions consistently to the correct account codes. This creates a cache of data that the business owner can use to make decisions for the future, based on what has happened in the business previously.

Once you have accurate historical data, you can start predicting or forecasting what’s going to happen in the future, and while most small businesses are good at compliance, they are pretty average at tracking profitability of different products / revenue streams, and they usually don’t do any forecasting at all (which is a lost opportunity for those businesses looking to grow).

Now that you’ve got an idea of the high-level role of the accounting team, let’s take a look at each of the players…

The CEO / Business Owner

The significance of this role in the accounting team is often overlooked. The role of the CEO or business owner is to understand the financial reports that are coming out of the business, and to make decisions based on those reports.

Business owners often think that because they have an accountant, they don’t need to be involved in the finances at all — but that’s very shortsighted. The role of the accountant is to provide information, and the CEO has a responsibility to understand those reports.

The owner/CEO really needs to understand their Profit and Loss statements, their Balance Sheet, the budget vs actual reports, and their cash flow forecasts. If they don’t understand those reports, their accountant should be talking them through it.

(It might take a few months of having your accountant explain your reports in detail for it all to make sense. However this is time well spent, as it is critical that the leader of the business is able to look at the Profit and Loss, Balance Sheet and Cash Flow Forecast and be able to tell the story of what has been happening in the business for that reporting period and what is expected to happen in coming months.)

It is important that the owner can look critically at these reports, too, because they will know all kinds of things that the accountant doesn’t.

For example, if your accountant is freaking out that your Profit and Loss report shows a cost of $10,000 more than the previous month, you will be able to explain that actually, you spent that $10,000 on a marketing campaign last month — it’s not like something got out of control or is going to be an ongoing expense.

It’s also important that you know what you are expecting to see in each report. If you signed a big client, but their payment isn’t reflected in your Profit and Loss report, you’ll know that something isn’t working in your reporting. Keeping a close, critical eye on the financial data of your business effectively gives you a pulse on the health of your business.

Key reports for the CEO to look at monthly include:

- Profit & loss statement (both a 1-page summary & a detailed report)

- Balance sheet (amount of money in each account, any loans, money owed by debtors and money owed to suppliers — most errors occur here.)

- Budget / Actual comparison (profit and loss)

In small business, the CEO should also be aware of the key compliance deadlines. The CEO is responsible for the business as a whole, and so they should have some kind of feel for the key deadlines and arrange to have reports or updates about when items have been filed or completed so that nothing falls through the cracks.

Tax Accountant

The role of the tax accountant is pretty self-explanatory. Their role is to meet compliance deadlines and to provide advice on how to best structure the business to manage risks and minimize tax. They are responsible for collating all of the data to complete tax requirements, file taxes and handle all the tax-related communications for the business.

For example, if the business owner wants to draw money out of the business and pay themselves, there are tax-effective ways of doing it (and ways that are very non tax-effective).

Other decisions the tax accountant can help with include conversations about which country the business should be set up in, and what structure should be used. They should also advise on tax planning strategies before the end of financial year to allow you to make any changes that will create a more effective tax situation for the business.

Related: 6 Tips for US Businesses to Take Advantage of 2016 EOFY and 7 powerful ways to minimise tax (legally)! – in Australia

.

Virtual CFO

A very large business will have the Chief Financial Officer (CFO) role set up in house, whereas small and mid-size businesses really can’t justify the cost of hiring someone full time, and so virtual CFOs are becoming more common.

The role of the virtual CFO is to ensure that the accounting data coming out of the business is accurate and relevant reports are being delivered, but also to think strategically taking into account both growth and risk management goals.

The CFO tells the story behind the numbers and helps the business to use the numbers to make decisions. It is their role to understand the business and the industry, understand the people in the business and their information needs, and then put it all together.

The virtual CFO is there to help people within the business make decisions based on accurate data and to look critically at the business and question what is and isn’t working.

The best way for businesses of smaller sizes to access this skillset is to engage a CFO for short periods of time — they don’t need high-level strategic advice full-time. A CFO might only be needed for a few hours a month, in businesses which need a clear, overarching financial strategy in order to keep growing.

For a small business (like most Bean Ninjas clients), the CFO will be preparing the cash flow forecast and budgets, as well as providing additional reporting for high-level financial decisions. They can provide a snapshot of where the business is at and how things are trending, as well as advising on future planning, strategic management and creating dashboards for tracking progress.

Bookkeeper

The bookkeeper’s role is to handle the day to day transactions in the accounting software and to make sure that each item is allocated correctly to the right account in the chart of accounts.

(This is a surprisingly important function: the tracking of transactions must be consistent for the rest of the financial reports to be accurate. If things are recorded inconsistently or inaccurately, it creates a ripple effect of mistakes through the financial apparatus of your business.)

Related: 10 questions to ask before you hire a bookkeeper

.

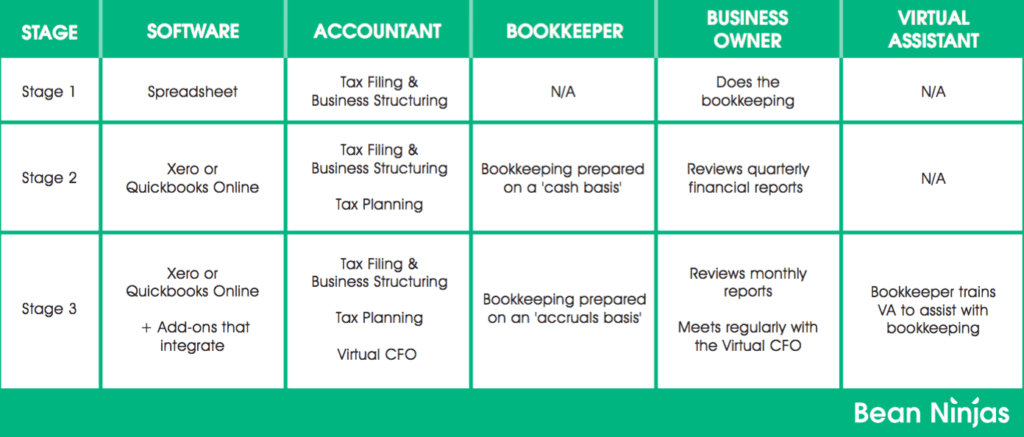

The Best Accounting Combinations for Each Stage of Growth

.Now, there are a number of different combinations of these roles that online businesses can use, and in the section below we’re going to work through the combinations that work best as your business grows.

.

Founder + Tax Accountant

Usually, the founder starts out solo and handles everything themselves for a while. Once they realise that they need help handling their tax compliance and tax returns, they engage an accountant. The Founder + Tax Accountant combination works well for early stage businesses and freelancers. As a business grows there are benefits in some of the other accounting team combinations.

.

Founder + Tax Accountant + Virtual Assistant (not recommended)

Then when the founder realize that day-to-day bookkeeping is taking up too much of their time, or is getting beyond their skill level, they either engage a bookkeeper or Virtual Assistant (VA). The problem with VAs at this stage is that bookkeeping is a specialized skill — many people have an accounting degree to do it — and a lot of errors are often made by VAs.

This means that the reports end up being incorrect and decisions are made based on inaccurate data. Alternatively the tax accountant has to be paid at a higher hourly rate than you would pay a bookkeeper to fix it all up at the end of the year.

The founder + Tax Accountant + VA combo is generally not a good one.

.

Founder + Tax Accountant + Bookkeeper

The next stage of building an accounting team is Founder + Tax Accountant + Bookkeeper. This is a good combination and should be the goal for most online businesses — a skilled bookkeeper should set up the accounting software and make sure that everything is accurate and efficient.

This will also ensure your tax accountant doesn’t need to charge additional fees when they prepare the tax return, because everything has been done correctly during the year. The tax accountant won’t need to fix anything and can just make a few tax adjustments and file the tax return(s).

.

Founder + Tax Accountant + Bookkeeper + VCFO + VA

As the business grows the owner will want more detail in the accounting software.

At this stage of the business, there will often be a larger volume of transactions to be processed by the bookkeeper. It now makes sense to involve a VA in the process to help with the administrative workload. The VA’s work should be reviewed by the bookkeeper.

It is usually around this stage that most businesses will also add a virtual CFO to the mix. This is the point at which forecasting becomes important, and where strategic financial opportunities start emerging and need careful expert attention to take advantage of them.

If you’ve got questions about how to structure the accounting team for your specific business, or about how to find a tax accountant or virtual CFO feel free to reach out for recommendations. Or if you’re looking for help with online bookkeeping, take a look at what we offer and get in touch! We’d love to help you secure the financial growth of your business.

Hiring an eCommerce accountant related articles

- How to hire and vet an ecommerce accountant

- 10 Questions to Ask Before You Hire a Bookkeeper

- What kind of financial leader do you need: Strategic vs. Operational Finance?

- What Does a Financial Controller Do?

- What to look for when choosing an eCommerce CPA

- What exactly does an eCommerce accountant do?

- Who Do You Need on Your Accounting Team?

- What to look for when choosing an accountant for your Shopify business

- When to hire a vCFO

- Working with a Bookkeeper: How to Get the Most Value Out of Your Bookkeeper